Ranking of Chinese Lithium Battery Companies

Ranking of Chinese Lithium Battery Companies

The ranking of Chinese lithium battery companies can be evaluated across multiple dimensions. Based on the latest market trends and industry data from 2024 and 2025, the major companies performed as follows:

I. Comprehensive Strength and Market Share

1. Power Battery Sector

-

CATL (Contemporary Amperex Technology Co., Limited):

For eight consecutive years, CATL has ranked first globally in power battery installation. In 2024, its global installed capacity reached 339.3 GWh with a 37.9% market share. Its Shenxing Battery (4C ultra-fast charging LFP) and Qilin Battery (CTP 3.0) have entered large-scale production. Mass production of solid-state batteries is planned for 2026. In China, its market share reached 46.2% in the first eight months of 2024. Clients include Tesla, BMW, NIO, and other global automakers. -

BYD:

In 2024, BYD’s installed power battery capacity was 153.7 GWh, ranking second globally with a market share of 17.2%. Relying on its proprietary Blade Battery technology (energy density of 180 Wh/kg) and vertically integrated model, BYD supplies mainly internally, but also externally to companies like Tesla and Toyota. The second-generation Blade Battery has increased density to 190 Wh/kg, enabling vehicles to exceed 1,000 km range. -

CALB (China Aviation Lithium Battery):

In 2024, CALB’s global installed capacity reached 39.4 GWh, ranking fourth with a 4.4% market share. The company focuses on “Infinity” solid-state battery tech and low-altitude economy scenarios, with battery installations for over 1,000 electric vessels.

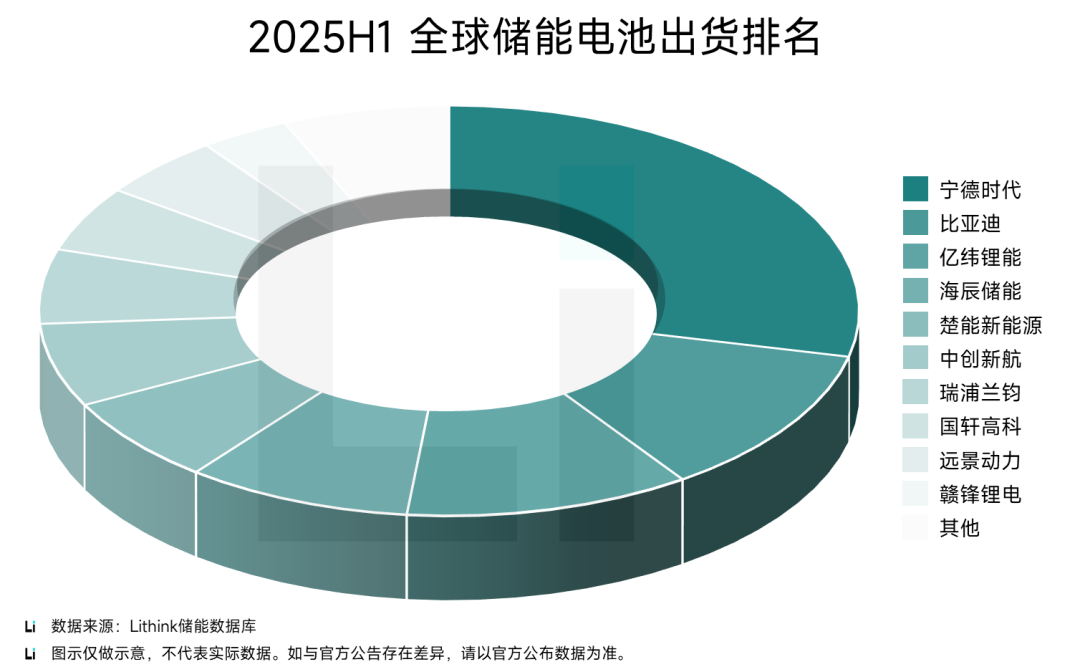

2. Energy Storage Battery Sector

-

CATL:

In 2024, CATL shipped nearly 110 GWh of energy storage lithium batteries globally, leading the market with a 29.5% share. In Q1 2025, it accounted for 30.7% of global shipments, topping both the AC side (system integration) and DC side (battery cells). -

EVE Energy:

In 2024, it surpassed BYD to become the second-largest global energy storage battery supplier. In Q1 2025, it held a 13.2% share in energy storage cell shipments. EVE covers consumer, power, and storage batteries, with overseas clients including Daimler and BMW. -

Hithium:

Ranked third globally in 2024 for energy storage shipments. In Q1 2025, it ranked third on the DC side, focusing on long-duration storage and overseas markets.

II. Financial and R&D Competitiveness

1. Revenue and Profit (Public Companies)

-

CATL:

2024 revenue: RMB 362.013 billion; net profit: RMB 50.745 billion; capacity utilization: 76.33%. R&D investment reached RMB 18.61 billion (industry second). -

BYD:

2024 revenue: RMB 777.102 billion; net profit: RMB 40.254 billion; R&D investment: RMB 54.16 billion (including battery business), leading the industry. -

EVE Energy:

2024 revenue: RMB 48.615 billion; net profit: RMB 4.076 billion; capacity utilization: 86.56%; R&D investment: RMB 2.942 billion.

2. R&D Investment and Technological Advancements

-

CATL:

Leads in high-energy-density materials, solid-state batteries (targeting 400 Wh/kg), and sodium-ion batteries. In 2024, R&D personnel exceeded 20,000, with 27.8% holding a master’s degree or higher. -

BYD:

Globally leading Blade Battery tech. In 2024, the company filed 217 patents related to solid-state batteries. Significant progress made in second-generation Blade Battery development. -

Sunwoda:

Plans to mass-produce full solid-state batteries (320 Wh/kg) by 2026, with costs dropping below RMB 2/Wh. Skips semi-solid solutions, directly focusing on sulfide electrolytes.

III. Global Expansion and Emerging Markets

1. Overseas Production Capacity

-

CATL:

Production bases include Thuringia, Germany (14 GWh), Hungary (planned 100 GWh), and Mexico (for North America). Overseas capacity is expected to exceed 30% by 2025. -

Envision AESC:

Operates 13 global bases across Japan, the US, the UK, and Spain. Ranked third globally in 2024 for energy storage exports. Its high-capacity battery cells are certified in multiple countries. -

Gotion High-Tech:

Göttingen base in Germany (20 GWh) went into operation, supplying Volkswagen, Bosch, etc. Overseas revenue share rose to 15% in 2024.

2. Emerging Application Scenarios

-

CALB:

Collaborated with XPeng Huitian on low-altitude economy batteries. Rail transport batteries tested to withstand over 5000V, passing 90 certifications from the China Academy of Railway Sciences. -

Rept Battero Energy (Chuneng New Energy):

Ranked 8th globally for energy storage shipments in 2024. Focuses on utility-scale energy storage, with over 500 GWh of planned capacity.

IV. Policy and Market Trends

1. Domestic Policy Drivers

-

NEV to the Countryside:

In 2025, 124 vehicle models are included in the subsidy catalog. BYD Han and CATL-equipped models saw significant sales growth. Rural NEV penetration rate rose to 27.2%. -

Energy Storage Subsidies:

China's storage market is expected to grow by over 50% in 2025. For the first time, overseas demand has surpassed domestic, boosting exports for CATL, EVE, and others.

2. International Competitive Landscape

-

Chinese Dominance:

In 2024, six of the top 10 global power battery suppliers were Chinese companies, with a combined market share of 67.1%. All of the top 10 energy storage battery suppliers were Chinese, accounting for over 93% of the global market. -

Decline of Korean/Japanese Players:

LG Energy Solution and Samsung SDI dropped out of the top 10 in energy storage. Chinese firms are rapidly gaining market share due to cost advantages and accelerated tech iteration.

V. Future Technology Focus

-

Mass Production of Solid-State Batteries:

CATL, BYD, and Sunwoda plan to commercialize solid-state batteries between 2026–2028, aiming for energy densities above 400 Wh/kg and costs at 50% of traditional lithium-ion batteries. -

Commercialization of Sodium-Ion Batteries:

CATL’s sodium-ion batteries have already been used in Chery EVs. 2025 production capacity is planned at 50 GWh, with costs 20% lower than LFP. -

Intelligent Manufacturing and Recycling:

CATL’s “lighthouse factory” has achieved 95% automation. BYD’s closed-loop battery recycling system recycles 95% of materials.

VI. Risks and Challenges

-

Overcapacity:

In 2024, China’s power battery capacity utilization dropped below 60%, putting pressure on some second-tier firms to exit the market. -

Raw Material Price Volatility:

Lithium carbonate prices fell 70% from 2023 highs, impacting profit stability. -

Technology Disruption:

Emerging technologies such as solid-state and hydrogen fuel cells may disrupt the current landscape, requiring sustained R&D investment.

Summary

CATL and BYD remain the top-tier leaders due to their vertically integrated operations and strong technological foundation. EVE Energy and CALB are rising rapidly in niche markets. Future competition will center around technological breakthroughs (e.g., solid-state batteries), global expansion (localized overseas capacity and services), and emerging applications (low-altitude economy, marine electrification). Companies must balance capacity growth with innovation investment to adapt to market uncertainties and policy shifts.