The era of battery cell wars has begun — Sungrow and CATL face off

Sungrow vs. CATL: The Battery Cell Wars Have Begun!

Sungrow and CATL—one is the king of energy storage, known for its system integration and deep expertise in power electronics; the other is the undisputed leader in the lithium battery supply chain. Now, they are finally facing off directly in the battery cell arena!

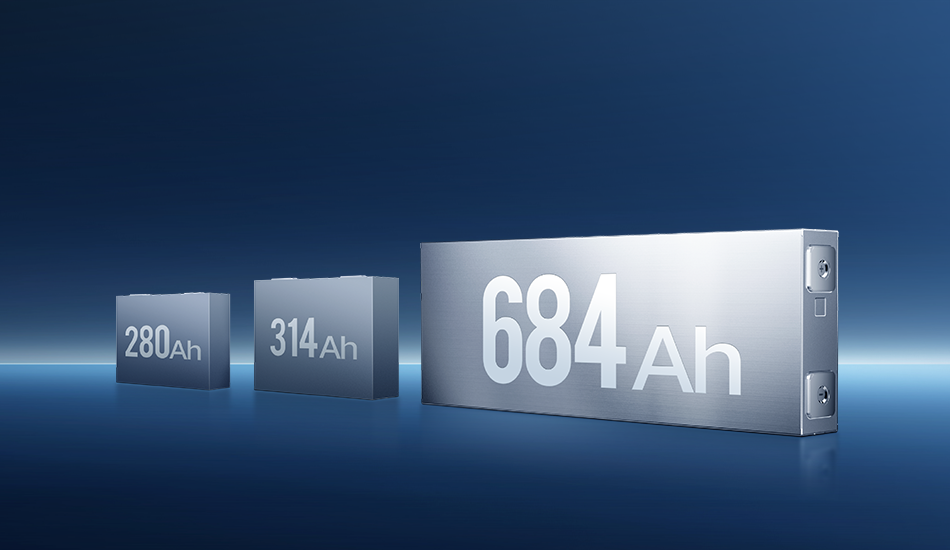

After 280Ah and 314Ah, battery cell specifications have entered a chaotic "Warring States" era—392Ah, 472Ah, 587Ah, 625Ah, 628Ah, 684Ah, 770Ah, 783Ah, 1175Ah… Capacities are getting larger, and types are multiplying.

Almost every player in the market understands one thing clearly: this period of fierce competition and wild diversification is only temporary. In the end, large-format battery cells will converge toward a unified standard. But every participant also hopes that their chosen specification becomes the benchmark—their product becomes the ultimate winner and the future mainstream.

This is a clash of titans: Sungrow vs. CATL. Don’t assume scale alone decides everything—Sungrow plays tough and speaks softly. Just look at how it has fiercely competed with Huawei in the inverter space for years.

So, how do you win this game?

First, with technology.

Second, with influence.

Third, through alliances.

At this point, the story starts to sound familiar. Isn’t this just like the solar wafer size battles we saw yesterday in the PV industry?

Battery cells are now repeating the story of solar energy.

But just because history repeats—

Does that mean it’s the right path?

Who Should Define Battery Cells?

Public data shows that many leading battery manufacturers are actively laying out their strategies and have launched their own large-capacity cell models. Since 2024, more than a dozen energy storage battery cell products with capacities over 500Ah have been introduced by top-tier and second-tier manufacturers. These include a wide range of specifications such as 530Ah, 565Ah, 587Ah, 625Ah, 628Ah, 630Ah, 688Ah, 690Ah, 720Ah, 770Ah, 1130Ah, and 1175Ah.

In addition to traditional battery makers like CATL, EVE Energy, and Sunwoda, the lineup also includes leading energy storage companies such as Sungrow, as well as ambitious new players like CRRC Zhuzhou Institute, known for its aggressive expansion.

On June 5, Sungrow officially announced that it has established the 684Ah cell specification as the next-generation large-format battery cell technology route, launching the PowerTitan 3.0 AC intelligent energy storage platform globally.

In its press release, Sungrow declared that this product release represents a new benchmark in defining battery cells. The 684Ah cell is the industry’s first large-format battery that can be mass-produced, using a dedicated stacking process, achieving a cycle life of over 15,000 cycles and pushing energy density to above 440Wh/L.

Sungrow emphasized that large-format cells impose higher safety requirements. To address this, it pioneered a thermal-electrical separation technology, redesigned exhaust ducts for directional heat discharge, and added a patented insulation layer to prevent the spread of exhaust and heat conduction—thus avoiding thermal runaway propagation.

Notably:

-

Sungrow does not manufacture cells itself—but it designs them. The energy storage sector is already fiercely competitive, and cell production involves heavy capital investment, which makes it unnecessary for Sungrow to manufacture in-house. The 684Ah cell product was developed in collaboration with downstream battery manufacturers.

-

Sungrow is a major buyer of battery cells.

In 2024, Sungrow shipped 147GW of PV inverters and 28GWh of energy storage systems globally. Compared to cell manufacturers, Sungrow’s strength lies in its deep understanding of market demand, as it can work backward from application scenarios and system-level requirements to define customer needs. This is why, in recent years, Sungrow has significantly increased investment in cell research and testing and has deepened its collaborative R&D with upstream suppliers.

Second- and third-tier battery makers may adopt the 684Ah standard due to Sungrow’s massive order volume. However, leading cell manufacturers and Sungrow’s competitors in the energy storage space may not necessarily “follow” Sungrow’s lead. The least likely to align with Sungrow is, unsurprisingly, CATL (Contemporary Amperex Technology Co. Limited).

CATL’s dominance in the battery industry cannot be ignored. According to data from Korean battery and energy research firm SNE, CATL held a global market share of 36.5% in energy storage cell shipments in 2024, maintaining the top spot for four consecutive years. CATL shipped 93GWh of energy storage systems in 2024, generating approximately 57.29 billion RMB in revenue from this business, accounting for 15.83% of its total revenue.

CATL’s technological prowess, market presence, and brand reputation need no elaboration. It has long led the cell market, shaping both technology pathways and industry trends. Its dominant market position is virtually unshakable. From CATL’s perspective, it alone may feel entitled to define the ultimate battery cell standard, while others’ efforts could be seen merely as challenges to its authority.

And given its characteristically assertive approach, CATL is unlikely to yield.

On June 10, CATL held its “Energy Storage 587 Technology Day” and officially announced the mass production and delivery of its 587Ah battery cell.

Naturally, CATL also claimed that the 587Ah cell is the optimal solution for next-generation energy storage. At the same time, the company noted that even larger-capacity cells are on the way—587Ah will be produced stably for a period, after which newer technologies will be introduced for the next iteration.

In this regard, CATL is actually quite similar to Sungrow. Last year in the second half, Sungrow announced a 625Ah cell, and now it has released a 684Ah version. In short, both companies are moving toward larger and larger cell capacities. The battery cells they introduce are always promoted as the best available for now, but clearly not the final form.

(Quick side note: Almost everyone says that “bigger isn’t always better” when it comes to battery cells—but where exactly is the limit?)

In addition, traditional cell manufacturers like EVE Energy, CALB, Sunwoda, and SVOLT have also released their own large-capacity cells. If we’re just comparing by size, HyperStrong stands out with its massive 1175Ah battery cell.

Sungrow’s competitors have also pushed back against its approach. For example, CRRC Zhuzhou, which in recent years has aggressively grabbed market share in energy storage through low-price bidding and by rallying a group of third- and fourth-tier battery cell suppliers around it.

CRRC Zhuzhou has also teamed up with downstream partners to launch its own “defined” cell. At the SNEC exhibition, state-owned enterprise Lishen showcased a 600Ah cell, claiming it was co-developed with CRRC Zhuzhou and will be exclusively supplied to them in the future.

In summary, the current battle over large-format cell standards is no longer just a competition between battery cell manufacturers—it's become a full-scale turf war involving energy storage companies and system integrators as well.

02. The So-Called "Technical Route Dispute" Is an Illusion — It's All About Commercial Competition

At the core, the trend toward larger battery cells is driven by one key factor: cost reduction.

This mirrors what happened in the solar industry with larger-sized silicon wafers. Using higher-capacity cells reduces the total number of cells required in an energy storage system, directly cutting costs.

When EVE Energy’s 60GWh super energy storage factory went into production, it highlighted the manufacturing of its 628Ah ultra-large cell, Mr. Big:

The production line outputs 1.5 cells per second from raw materials to finished product, assembles four complete battery packs per minute, and can produce more than 40 containers’ worth—equal to 5MWh—per day.

Large-scale, high-efficiency production significantly lowers per-unit manufacturing costs.

With larger cell capacities, the total number of cells required per system decreases. As a result, the number of supporting components—like cables, battery management systems (BMS), and monitoring units—also shrinks, which further reduces material costs.

In addition, fewer parts mean faster assembly and lower labor costs.

As noted in EVE Energy’s investor communication on April 19, 2024:

“In April 2025, we’ll launch a 6.9MWh energy storage system based on large cell technology and highly integrated CTP (cell-to-pack) design. This will reduce pack costs by 10% and increase energy density per unit area by 20%.”

Secondly, advances in industry-wide technology are enabling the development of larger cells:

Higher energy density, better materials, smarter structural designs.

With improved materials and optimized architecture, energy density increases even within the same physical dimensions.

These large-capacity cells are often designed and manufactured using cutting-edge technologies, achieving superior performance in lifespan, charge/discharge efficiency, and reliability.

Third, the move to larger cells is also a response to evolving market demands, particularly the rise of long-duration energy storage (typically defined as storage lasting 4 hours or more).

Large-capacity cells are naturally well-suited for such use cases. For example, HyperStrong’s 1130Ah cell was designed specifically for long-duration storage applications—offering high energy and high capacity to match the market's needs.

All of the above are common industry talking points, publicly stated by companies as justification.

But in the view of GanTanHao (赶碳号), the battle over cell specifications is fundamentally about control—a battle over who holds the narrative and dominance in the energy storage sector.

① Branding, Independence & the Illusion of Innovation

In this free-for-all over cell formats, companies often launch “customized” or proprietary specifications to signal technological independence and leadership.

Even if the actual tech isn’t particularly advanced, loud marketing and strong visibility help them shape perception and show that they’re still in the game.

Some companies—like REPT BATTERO, known for competing purely on price—seem more focused on visibility than genuine technical leadership.

That’s why at trade shows like SNEC, you’ll often see booths displaying a dozen different cell specifications. But in reality, most of their production still revolves around 280Ah and 314Ah.

The rest are just concepts, roadmaps, or paper specs.

② Why Switching to Large Cells Isn’t So Simple

Upgrading a production line from smaller to larger cells isn’t cheap—it requires investment in:

-

Equipment updates

-

Process reconfiguration

-

Workforce retraining

If a manufacturer transitions from wound to stacked cells, the equipment overhaul alone is massive.

This isn’t as brutal as in the PV industry, where a mono furnace built for 182mm silicon wafers simply cannot pull 210mm wafers due to chamber diameter limitations—only incremental steps like 183mm or 191mm are possible.

Still, for cell makers, the capital required to retool at scale is considerable. Hence, most companies are very cautious about production line upgrades.

They don’t change easily—which is exactly why so many companies loudly proclaim their chosen spec is the best, hoping others will follow their lead, phase out old lines, and unify around their standard.

Deep down, everyone knows:

“If your rival has to pause, spend, or switch—it's your chance to surge ahead.”

③ Smaller Players Are Being “Forced” to Choose

At the just-concluded SNEC expo, REPT BATTERO also launched a 684Ah cell, clearly targeting Sungrow as its key customer.

One booth staffer said:

“The cost to upgrade our lines is high. That’s why in this partnership, Sungrow is underwriting the production line investment.”

This reflects both the pressures smaller players face, and the growing influence of Sungrow in shaping the future of cell standards.

Epilogue: A Familiar Story

“What experience and history teach is this—that nations and governments have never learned anything from history.”

— Hegel

This quote fits today’s solar and energy storage industries all too well.

The cutthroat chaos and vicious price wars that plagued the PV sector should serve as a serious warning to the energy storage world.

But in reality, energy storage seems destined to walk the same path—and maybe even worse. The mistakes of PV will likely be repeated, not avoided.

Just as the solar wafer size war began in 2019 and lasted until 2024, involving nearly every major PV company,

how long will the large battery cell war last?

Some companies—knowing full well they’re unlikely to win—still throw everything into the fight, trying to grab their share of the future.

Fierce, cutthroat competition seems to be the default setting of China’s new energy sector.

But let’s be clear:

It’s not that Chinese energy companies lack innovation or strength.

It’s the hyper-aggressive environment that makes the fight so brutal.

So—who’s to blame?